CloserStill and Nineteen Group chairman Phil Soar looks at two independent studies shining a light on the largest organisers operating from the UK today.

Which are the largest exhibition groups in the UK? We get this question a lot – it’s easy to ask and difficult to answer. Unlike most other industries, there is barely ever a “Top 100” article about our businesses anywhere.

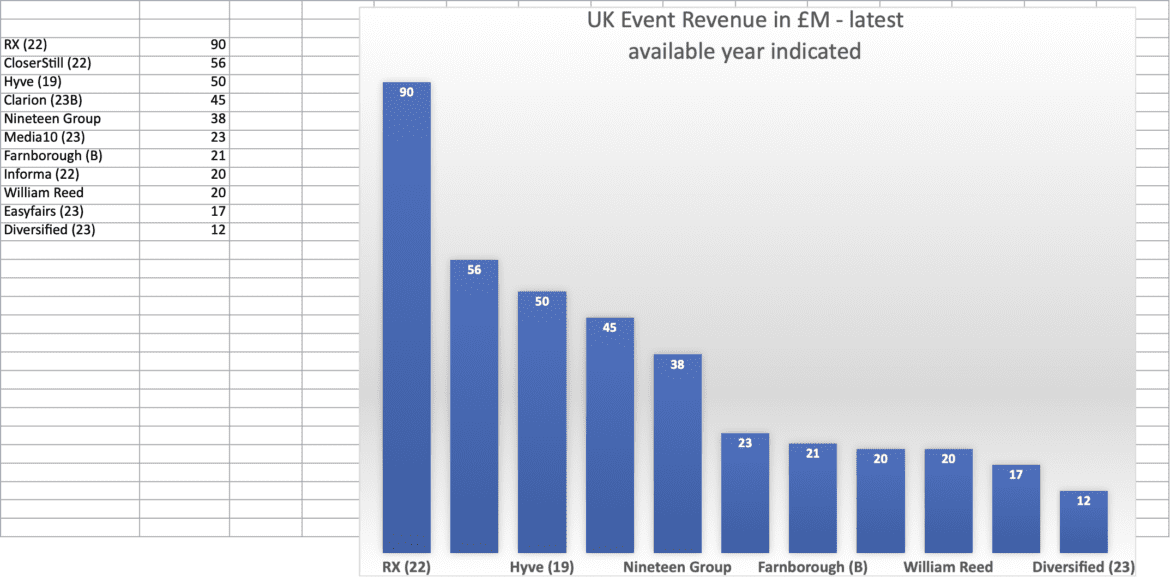

Below is independent research by Plural Strategy covering the companies with the largest annual exhibition turnover in the UK.

There are several caveats. The numbers are based on annual reports, Companies House filings and public pronouncements in the period from 2019 to early 2024.

The year of the latest info is given on the graph below. Where there is no year stated, the numbers are Plural’s estimate from recent statements (some companies don’t always isolate UK turnover from worldwide numbers). Hence, this is a very well-researched “best estimate” but it cannot be perfect.

In the case of both Clarion (DSEi being its biggest event) and Farnborough (with the Air Show), allowance has been made to “smooth” these large biennials – otherwise an “on” year would show far higher revenue than an “off” year. (Hence the letter B). In addition, Clarion’s second largest UK event, ICE will now be staged in Barcelona.

Note also that not all companies have 31 December year ends – these numbers are all for a single 12-month period, but not the same 12 months in every case.

The difficulties of isolating only UK revenues

The material has been prepared by Plural as part of its ongoing and continually updated analysis of the market.

What is immediately striking is how small the UK turnover is compared with the total size of each of these businesses.

Informa’s UK turnover is less than 1% of its worldwide sales. RX’s is circa 7% of worldwide sales, Clarion’s is perhaps 9%. Even CloserStill, which had zero non-UK turnover at all for the first half of its life, now has 72% of sales outside its home market.

CloserStill is a surprising number two as it does not have a £20m+ behemoth (Clarion has DSEi, Hyve has Spring and Autumn Fair, RX has WTM).

CloserStill has no show with an eight-figure turnover but does have seven events turning over more than £4m in the UK alone, only one of which was acquired.

Nineteen, having been founded only in 2018, owes its place to the massive growth of Safety and Security, Installer and Retail Technology.

Informa/UBM would probably have topped the table ten years ago with Interiors, EcoBuild, IFSEC, IPEX and others but has reduced its efforts in the UK.

Media10 is the only mainly consumer show organiser in this list of 11. This again shows how the world has changed in the past 10-15 years. A list of the top dozen in 2010 would certainly have contained SMMT (Motor Show), the Boat Shows and other consumer organisers such as Brand Events and BBC/Haymarket.

What about worldwide turnover?

Colin Morrison, owner of Flashes and Flames, has taken an increasing interest in the sector in recent years and has a solid, objective view. Incidentally, if you are interested in the media world and exhibitions in particular, and you don’t read Flashes and Flames, you should. You will learn more there than from any other source (apart from EN of course).

Morrison has recently looked at our industry and, knowing all these businesses, he has created his own analysis and rankings.

What’s valuable about his summary is that he has excluded all of the exhibition operations, owned and run by countries, regions and cities – the reason being that they are never going to be sold on any open market, their objectives are not comparable, they are not shareholder orientated, and it is almost impossible to extricate exhibition revenues from all the other venue turnover.

This then excludes the Italian, Spanish and German Fiera/Messen and companies like Comexposium, which since its bankruptcy is owned by French state players (Compexposium would rank third or fourth if included).

Below are Morrison’s findings and assumptions, in order of size.

The number is the annual turnover in sterling for a single 12 months, in the period 2021-24, depending on the latest data available.

Inevitably, therefore, there is bound to be some estimation in the numbers as some may be even two years out of date.

- 1. Informa Markets £1.7 billion

- 2. RX (Reed) £1.3 billion

- 3. Clarion £500 million

- 4. Emerald £349 million

- 5. CloserStill £202 million

- 6. Hyve £195 million

- 7. Easyfairs (inc venues) £188 million

- 8. Ascential * £180 million

- 9. DMG £150 million

- 10. ARC £150 million

- 11. Terrapin £98 million

- 12. Questex £95 million

*Ascential has now been detached from the other parts of its old group and is solely Cannes Lions and Money 20/20. It has not produced accounts since that occurred.

Coming after these twelve are a small number of reasonably-sized companies. Several are still family-controlled or managed – Mark Allen, William Reed, Terrapinn and Montgomery. Then, there are a small number of fast-growing businesses in the £30-50m range – e.g. Media10 and Nineteen.

The list attempts to include only trade show/exhibition groups and excludes companies which are essentially conference-led. It also does not include trade association events in the US, which can be quite large but are single.

It is striking how different this list is from the same presentation of 1999/2000 – a quarter century ago. That would have been dominated by Reed, EMAP, Penton, VNU, DMG, UBM and Comdex – the first six all being publicly listed companies.

Size doesn’t necessarily translate to value

Morrison also draws assumptions about how valuable each of these companies are – and this does not necessarily relate to turnover. For instance, he speculates that Questex might be sold for US$550m, Clarion may be valued at £1.5bn and CloserStill at £1bn.

But Emerald, despite being the fourth largest organiser in terms of turnover, is, according to Morrison’s research worth US$600m at ‘enterprise value’ (that is the total value before taking off debt). Emerald has been talking to prospective buyers for several months and Morrison may have inside information on that process. Any business is worth only what someone will pay for it after all.

Debt is also a critical consideration for all of these companies. Morrison observes that ARC has spent £300m to acquire several assets from scratch – this is an excellent model, but it does mean that the amount of debt relative to turnover and profit will tend to be rather higher than for companies which have largely grown organically (like Terrapin, Easyfairs and CloserStill).

Morrison also speculates about what will happen to these companies in the reasonably near future. Except for Informa, he speculates that every single one of the 12 could be sold to future investors.

RX seems unlikely, and its ultimate sale has been under discussion for three decades. DMG is a valuable asset, but with the group now being privately owned and possibly seeking funds to buy the Daily Telegraph, any sale would be a long way off.

It would (we presume) be of interest to the industry to try to produce the “Top 20” or “30” UK organisers each year. We shall endeavour to work on that.

Source: www.exhibitionworld.co.uk

Comments are closed.